Breaking News

Stock Market

US Stocks Skyrocket in 2024: Analyzing Wall Street's High Hopes amid Investment Risks

Leo Gonzalez

March 10, 2024 - 12:27 pm

Wall Street Wonders: A Closer Look at the Soaring US Stocks Amid Boom-and-Bust Fears

In the wake of an extraordinary climb, US stocks have started the year 2024 on a high note, inviting a wave of both anticipation and apprehension across Wall Street. The S&P 500 Index’s repeated closing at record highs speaks to an economy marked by resilience and robust corporate earnings, but it raises an important question—is the US stock market overheating?

Unprecedented Rise of the S&P 500

So far this year, the S&P 500 Index has reached unprecedented highs, closing at record levels 16 times, which accounts for nearly a third of all trading days. Tech shares, particularly those in AI, have seen extraordinary gains; Nvidia Corp. is a stand-out, having surged by nearly 80% and adding about $1 trillion in market value before experiencing a minor retreat alongside other tech stocks on a recent Friday. Furthermore, historically speculative domains such as Bitcoin have also seen a resurgence in value.

Economic Stability Versus Speculative Frenzy

Despite these impressive records, some signs indicate that the market's strength is not solely the result of speculation gone wild. Not all heavy hitters in the stock market, commonly referred to as the "Magnificent Seven," have maintained a steady upward trajectory, suggesting investors are discerning rather than reckless with their investments. Additionally, the response to IPOs has been relatively subdued, further supporting the notion that we are not witnessing a speculative frenzy.

Even more reassuring is the new peak reached by an equal-weighted version of the S&P 500, signaling a more broad-based rally where gains are distributed more evenly across companies rather than being concentrated in a few oversized tech giants. Valuations for the most significant stocks in the benchmark index also remain relatively modest, especially when compared to the market leaders during the zenith of past market cycles.

The Tech Giants: A Mixed Bag of Fortunes

The Magnificent Seven, comprising Apple Inc., Alphabet Inc., Amazon.com Inc., Meta Platforms Inc., Microsoft Corp., Nvidia, and Tesla Inc., moved almost in lockstep throughout the previous year. They were the powerhouses behind the significant market gains and, until recently, the largest constituents of the S&P 500.

Scott Chronert of Citigroup Inc. underscores that these seven megacap tech firms contribute about 20% to the S&P 500's earnings—a substantial justification for their combined one-third market-capitalization weighting of the index. Moreover, Chronert draws parallels between the infrastructure-building periods of the Internet and AI but points to the contemporary, sturdy revenue models and cash flows as distinguishing factors.

Signs of Divergence among the Technology Titans

However, in 2024, the unanimity of these tech titans has shown some signs of fracturing. Investors are cooling off on the outlook for several of these companies, an indication that any perceived speculative bubble may be losing steam. For example, Apple Inc. underwent a decline partly due to concerns over iPhone sales in China. After reaching a record high in December, the company saw its stock value retreat. Meanwhile, Tesla Inc. has experienced a more significant downturn, with diminishing vehicle demand resulting in a dip in market value below that of Eli Lilly & Co. Alphabet Inc. has not been spared from this year's downward trend either.

Gains Shifting Beyond Technology

Although unease may persist over the concentration of stock advances in a few companies, the market expansion is starting to move past just technology firms. For the first time in two years, the S&P 500 Equal Weight Index, which assigns equivalent weight to each of its constituents regardless of market capitalization, set a closing record last week. This broadening participation is supported by a rise in the portion of S&P 500 stocks reaching all-time highs, reaching levels not seen since early 2022, according to Bloomberg Intelligence strategists Gina Martin Adams and Gillian Wolff.

Room for Growth in the Bull Market

Adams and Wolff suggest there could be ample space for the bull market to rally further, evidenced by less than a third of stocks currently boasting record levels. In contrast, during the culmination of the tech bubble nearly a quarter-century ago, the prevalence of stocks at such levels was dwindling.

The Subdued State of IPOs

Another factor tempering concerns over an overheated market is the measured interest in initial public offerings. Unlike the frenzy of 1999, when around 42% of US IPOs yielded a 50% price jump on the first trading day, in 2024 only CG Oncology Inc. managed to achieve this mark. IPO activity has substantially cooled down from the heights it reached in 2021, with this year observing 36 IPOs and a capital raise of $7.2 billion compared to the approximately $300 billion raised from around 1,000 deals in 2021.

A Comparative Look at Valuations

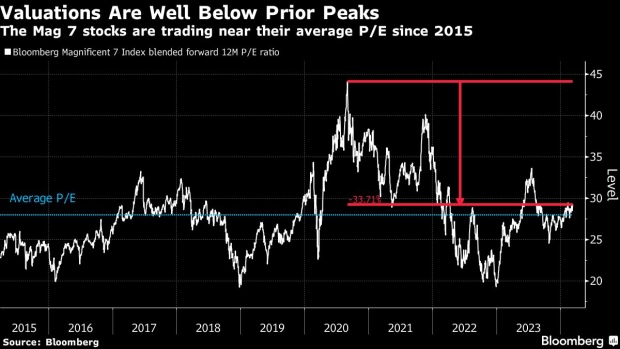

When reflecting on the tech behemoths’ profit margins, it is clear that the once stratospheric valuations have tempered. While remaining high, these valuations are substantially lower than previous historic peaks. For instance, the Magnificent Seven trade close to their average price-to-earnings ratio since 2015. Moreover, the largest five stocks in the S&P 500 now trade at less than half the price-to-earnings multiples seen in the top companies during the early 2000s tech bubble, such as Intel Corp., Cisco Systems Inc., Microsoft, and Dell.

Valuations also remain in check in other tech sectors, like AI and robotics, exhibiting price-to-sales ratios in line with or below the five-year average, as reported by Bloomberg Intelligence.

In a comprehensive analysis facilitated by experts including Elena Popina, Jessica Menton, and Bailey Lipschultz, Bloomberg L.P. provides a nuanced picture of the current market scenario. The array of charts and data available help dispel concerns of a bubble potentially forming, offering a more grounded view amid the spirited ascent of the US stock market.

The Bottom Line: Rational Exuberance or Cautionary Optimism?

As we navigate the impressive yet challenging terrain of 2024’s stock market, the line between an equitable growth spurt and an overzealous bubble grows fine. While the S&P 500's sterling performance raises eyebrows, the diversity of booming stocks and the more rational valuations provide a counterbalance to bubble fears.

Instead of reckless investment buoying only a select few, the market's rally appears more democratic. Technology, while still a prominent player, shares the stage with a gamut of industries enjoying their moment in the financial limelight. The signs of cooling in tech giants, coupled with a calmer IPO landscape, reflect a market mindful of past lessons.

Investor sentiment, though positive, seems mindful of the ephemeral nature of excess. A study of market history and valuation trends supports a movement toward more sustained and less speculative growth. While vigilance is often the price of economic prosperity, current market indicators suggest that optimism, for the time being, is well-founded.

As the S&P 500 continues to reach new summits, investors and spectators alike watch with bated breath, hoping the ascent is part of an enduring path upward rather than a prelude to a steep and unforgiving descent akin to past financial crises.

In summary, the financial market of 2024 reflects both a celebration of advancement and a cautious tale of moderation. While Nvidia’s exceptional performance and the S&P 500's record highs point to an era of prosperity, the evolution of the market’s composition, IPO interest, and tech valuations also speak to a more mature, potentially more stable, period of economic growth. Deploying insights from seasoned analysts and detailed data analysis, the market stands as a testament to the ever-changing tides of finance—a landscape where luxury and liability frequently intermingle.

Additional Information

To delve deeper into the current state of US stocks and the potential risks and rewards they represent, interested readers can explore the wealth of information available at Bloomberg.

Copyright © 2024 Bloomberg L.P. All Rights Reserved.

broadcast hub network© 2024 All Rights Reserved